Picture this: A surgery goes smoothly. The patient is discharged. Six weeks later, a bill arrives for $4,200 from a radiologist they never met, never selected, and had no way of knowing was out-of-network.

The facility was in-network. The surgeon was in-network. The radiologist, assigned automatically as part of the procedure, was not.

For health plans, that scenario carries more than a member service problem. It carries a cost-sharing obligation, a potential regulatory penalty, and a member who is now reconsidering their coverage at the next open enrollment.

Surprise billing is widely understood as a patient protection issue. What gets less attention is how much of it is preventable before any claim is ever filed, and how directly that prevention connects to the quality of a plan's provider data.

Here is what drives it, what the law requires, and where the operational fix actually lives.

What Surprise Billing Actually Is and How It Happens

A surprise medical bill is an unexpected charge from an out-of-network provider the patient had no reasonable opportunity to choose differently. It differs from a standard out-of-network charge, where the patient knowingly sought care outside their network. Surprise billing typically originates in one of four ways:

- An in-network facility assigns an out-of-network provider the patient did not select

- Emergency care is delivered at an out-of-network facility

- A member selects a provider listed as in-network whose status is actually incorrect

- An in-network referral leads downstream to an out-of-network specialist without the member realizing it.

The third scenario is where provider data quality becomes the direct driver of billing exposure, and the one plans have the most operational control over.

The Most Common Scenarios Health Plans Face

|

Scenario

|

How Exposure Is Created

|

Plan's Obligation

|

|

Out-of-network anesthesiologist at in-network facility

|

Member assumes in-network coverage

|

Cover at in-network cost-sharing; absorb the difference

|

|

Emergency care at out-of-network facility

|

Member had no alternative

|

Emergency services covered at in-network cost-sharing

|

|

Directory lists an out-of-network provider as in-network

|

Member relies on inaccurate data

|

Plan bears cost-sharing liability

|

|

In-network referral leads to out-of-network lab or specialist

|

Member unaware of the transition

|

Covered as in-network if no reasonable alternative existed

|

The directory inaccuracy scenario is the only one on this list that is entirely preventable before the member ever makes a call.

Why Surprise Bills Still Happen Four Years After the No Surprises Act

The No Surprises Act closed many billing pathways but did not fix the data conditions that produce surprise bills. Three root causes continue to drive complaints and disputes.

Contract lag: Providers join and leave networks continuously. When contracting and directory systems are not connected in real time, there is always a window where a provider's directory status does not reflect their actual contract status.

Delegated data failures: Provider groups submit roster files in inconsistent formats on their own schedules. Without automated validation, errors enter the directory and compound before anyone catches them.

Outreach frequency gaps: The No Surprises Act requires verification every 90 days and directory updates within two business days of any reported change. Plans still running annual verification cycles are both out of compliance and carrying inaccuracy risk they are not measuring.

The Provider Directory Connection Most Plans Miss

Most conversations about surprise billing focus on resolution: the dispute process, arbitration, cost-sharing calculations. Those matter, but they address surprise bills after the damage is done.

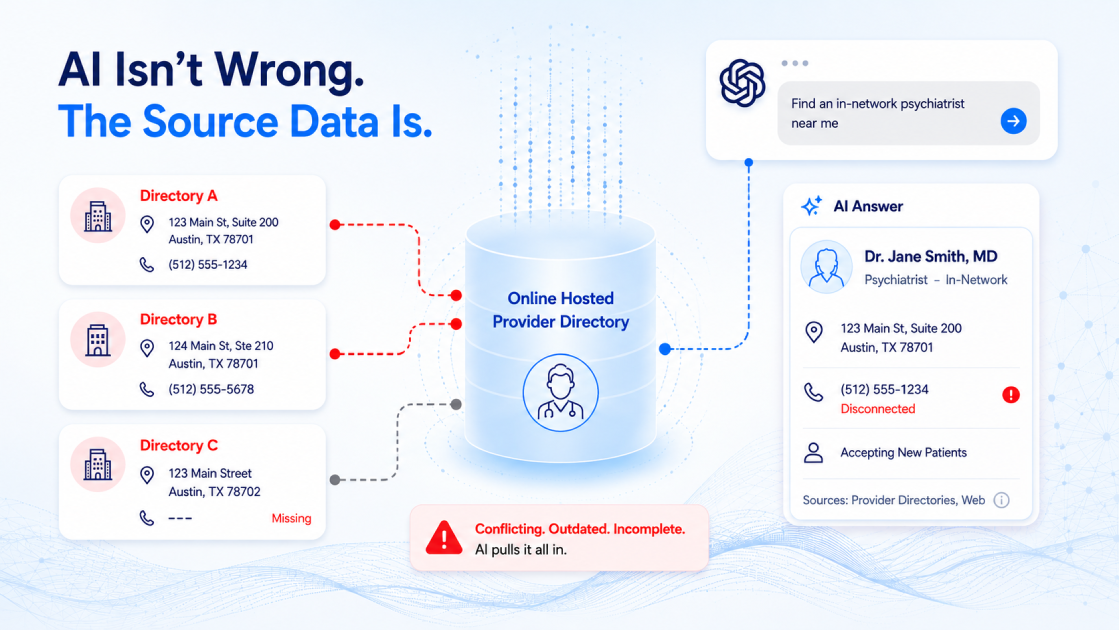

The upstream leverage point is the directory. A Senate subcommittee investigation found that one-third of provider listings contacted were inaccurate. When a member relies on that information and receives an out-of-network bill, the plan absorbs the cost-sharing difference.

Every inaccurate listing is a claims liability that never appeared in any risk model. According to Atlas Systems' 2025 Member Experience Monitor, 40% say that Google and other “alternative” sources have more accurate provider information than directories. The financial impact is immediate. The reputational damage compounds with every enrollment cycle.

What the Law Requires from Health Plans Today

Four obligations under the No Surprises Act directly reduce surprise billing exposure:

Hold harmless: In covered situations, plans limit member cost-sharing to the in-network amount and absorb the difference. This is not discretionary.

Provider directory accuracy: Verify every listing at least every 90 days, update records within two business days of a reported change, and remove unresponsive providers rather than leaving them in place.

Notice and consent: Balance billing is permitted in narrow non-emergency circumstances only with specific, voluntary, advance written consent obtained before the service.

Good Faith Estimates: Providers must supply uninsured patients with a written cost estimate before scheduled care. A proposed pre-service AEOB rule for insured patients remains pending as of early 2026.

Balance Billing vs. Surprise Billing: Understanding the Difference

| |

Balance Billing

|

Surprise Billing

|

|

What it is

|

Provider charges the gap between their full fee and what the plan paid

|

Patient receives an unexpected out-of-network bill they had no chance to avoid

|

|

Patient's knowledge

|

Patient chose or knew the provider was out-of-network

|

Patient had no reasonable opportunity to know

|

|

NSA protection

|

Not automatically prohibited; depends on context

|

Prohibited for emergency care, covered ancillary services, and air ambulance

|

Balance billing is a billing method. Surprise billing is the patient experience that results when it occurs in a protected situation without informed consent.

The Financial and Reputational Cost to Health Plans

Surprise billing exposure extends well past paying the claim. The downstream costs are real and consistently undercounted.

Claims liability: Directory-driven out-of-network services mean the plan covers cost-sharing it never modeled for. Systematic data failures create material financial exposure at scale.

Regulatory penalties: Violations can result in civil monetary penalties of up to $10,000 per incident, along with federal audits and corrective action plans.

Member retention: Atlas Systems' 2025 Member Experience Monitor found that 80% of members who encountered a directory error trusted their health plan less as a result. Members who receive an unexpected bill tied to a directory error do not renew quietly.

What CMS-4208-F2 and the REAL Health Providers Act Add to the Picture

For plans managing Medicare Advantage business, surprise billing risk now extends into how directory data performs publicly on Medicare Plan Finder. Inaccurate listings mean members enroll based on a network that does not reflect reality, then encounter the gap when they seek care.

The REAL Health Providers Act's cost-sharing liability provision, effective plan year 2028, converts each of those directory failures into a direct claims obligation.

Building the Operational Controls That Actually Prevent It

Prevention requires controls that surface inaccuracies before they reach any member. Three capabilities define what that looks like:

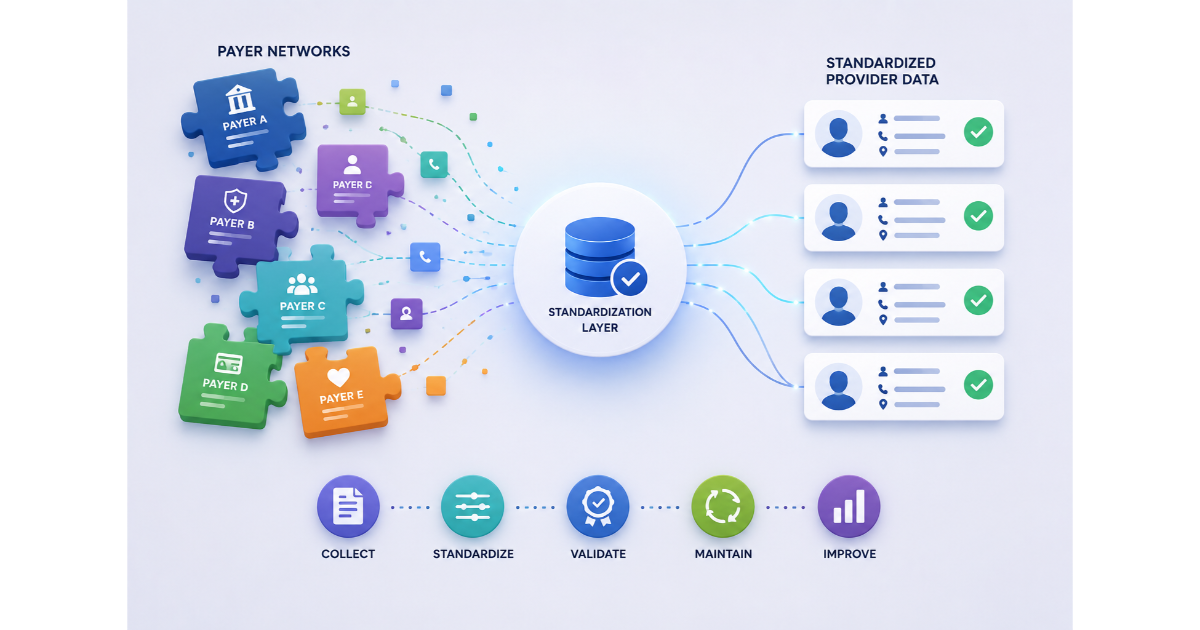

- Upstream data normalization: When delegated roster files arrive in inconsistent formats, automated normalization resolves NPI mismatches, removes duplicates, and validates records before they enter the directory.

- Continuous verification: A 90-day cycle means tracking each provider record individually and triggering outreach before the window closes, not running a quarterly batch and calling it done.

- Real-time system connectivity: When a contract terminates, that status needs to reach the directory within days. Without a live connection between contracting and directory platforms, the lag between those two systems is where surprise billing originates.

A plan that discovers a directory problem through a member complaint is already downstream of the failure. PRIME® by Atlas Systems supports this kind of continuous data management: automated roster normalization, ongoing monitoring against live provider data, and real-time directory updates that close the gap before it reaches a member. See how PRIME® supports surprise billing prevention.

Get a demo today!

FAQs

What is surprise billing in healthcare?

Surprise billing occurs when a patient receives an unexpected charge from an out-of-network provider they did not knowingly choose. It most commonly happens during emergency care, when a facility assigns an out-of-network provider to an in-network procedure, or when a member selects a provider based on directory information that is inaccurate or outdated.

How does the No Surprises Act protect patients from surprise medical bills?

The law prohibits balance billing in emergency situations, for covered ancillary services at in-network facilities, and for out-of-network air ambulance services. In those situations, patients pay only their in-network cost-sharing. The plan absorbs the difference. Providers cannot balance bill without specific, voluntary, advance written consent in the narrow non-emergency circumstances where that exception applies.

What is the difference between surprise billing and balance billing?

Balance billing is the practice of billing a patient for the gap between the provider's full charge and what the plan paid. Surprise billing is what the patient experiences when that bill arrives unexpectedly from a provider they had no real opportunity to identify as out-of-network. All surprise bills involve balance billing, but not all balance billing constitutes a surprise bill under the law.

Are Medicare Advantage plans subject to surprise billing rules?

The No Surprises Act does not apply directly to Medicare Advantage plans, which have separate billing protections under Medicare. However, the REAL Health Providers Act extended the same directory accuracy standards to MA plans, and cost-sharing liability for directory-driven errors applies to MA beginning plan year 2028.

How can health plans reduce the risk of surprise billing complaints and litigation?

The most effective intervention happens before any bill is generated: running 90-day verification cycles on every provider record, normalizing delegated roster data before it enters the directory, and maintaining real-time connectivity between contracting and directory systems. Plans that build this infrastructure reduce directory-driven surprise billing at the source, before it generates claims liability, regulatory penalties, or member complaints.

.webp?width=387&height=387&name=Medtech%20Breakthrough%20Award%20Winner%20(1).webp)

.webp)

.png)